[ad_1]

So time for my typical evaluate of the yr. As ever, I’m not scripting this precisely on the finish of the yr so figures could also be a bit fuzzy, usually they’re fairly correct.

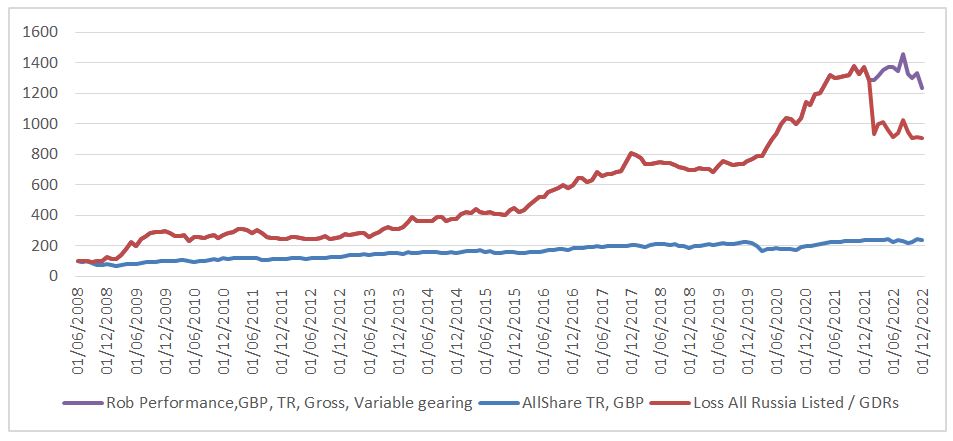

As anticipated, it hasn’t been one. If you happen to assume all my MOEX shares are price 0 I’m down 34%, in the event you take the MOEX shares at their present worth I’m down c10%. That is very tough, I even have varied GDR’s and an affordable weight in JEMA – previously JP Morgan Russian. So if all Russian shares are a 0 you’ll be able to most likely knock one other 3-5% off.

My conventional charts / desk are under – together with figures *roughly* assuming Russian holdings are price 0. It’s just a little extra advanced than this as there are fairly substantial dividends in a blocked account in Russia and fairly a couple of GDR’s valued at nominal values, I may simply be up 10-20% in the event you assume the world goes again to ‘regular’ and my property usually are not seized, though at current this appears a distant prospect.

We’ll see what occurs with the Russian holdings however I’m not optimistic. If the Ukraine warfare continues alongside its present path Russia will lose to superior Western know-how / Russian depleting their shares. The Russian view appears to be to have an extended drawn out warfare – profitable by attrition / weight of numbers / economics. The EU remains to be burning saved Russian gasoline, with restricted capability for resupply over the following two years, 2023/2024 could also be very tough. I don’t assume it will change the EU’s place nevertheless it may. One other probably approach this ends is nuclear / chemical weapons because it’s the one approach Russia can neutralise the Ukrainian / Western technological benefit. A coup / Putin being eliminated is one other risk, as is Chinese language resupply /improve of Russian know-how (although far, far much less probably). I believe the longer this continues the extra probably Russian reserves are seized to pay for reconstruction and western holdings are seized in retaliation. I nonetheless maintain JEMA (JPMorgan Rising Europe, Center East & Africa Securities) (previously often known as JP Morgan Russian) as I get a 5x return if we return to ‘regular’, 50% loss if property are seized. If you’re within the US and might’t purchase JEMA an identical, (however a lot, a lot worse) different is CEE (Central Europe and Russia Fund). I’d write about it if JP Morgan do one thing dodgy and power me to change. There’s some information suggesting 50% haircut – really a c2.5x return could be an honest win.

All of the above after all doesn’t indicate I assist the warfare in any approach. I all the time say this however shopping for second hand Russian shares does nothing to assist Putin / the warfare. Nothing I do modifications something in the actual world. For what it’s price, my most popular possibility could be to cease the warfare, present correct info on what has gone on to all ‘Ukranians’, let refugees again, put in worldwide screens / observers to make sure a good vote then have a verifiably free election asking them what nation they wish to be a part of, within the varied areas then respect the consequence. I’m conscious that they had an independence referendum in 1991 – however in addition they voted to stay within the USSR in 1991 too….

H2 has, if something been worse than H1. My coal shares have executed effectively however I can’t see them going a lot larger with coal being 5-10x greater than the historic pattern. I’ve bought down and am now operating the revenue. I’ve struggled with volatility and bought down some issues which looking back I remorse – notably SILJ (Junior Silver Miners) and COPX (Copper Miners). It’s partly as I believe we might be due a serious recession and far silver / copper demand is industrial. Nonetheless assume that these metals will do effectively as manufacturing could be very contstrained however I’m higher off avoiding fairness ETFs in future. I’m higher off in my typical space of grime low-cost equities – that I can think about and maintain. Situation is I discover it very, very tough to seek out useful resource shares that I really wish to spend money on.

I’m nonetheless at my restrict when it comes to pure useful resource shares, possibly the change from extra discretionary / industrial copper / silver to non-discretionary vitality will assist.

Power has executed fairly poorly, regardless of very low valuations. For instance Serica (SQZ) I’m c20% down on regardless of it having over half the market cap in money and forecast PE underneath 2/3. Its at the moment investigating a merger / takeover. I dislike the deal on a primary look however havent but totally run the numbers and don’t have full info.

PetroTal – once more executed poorly, down about 20% because of points in Peru, forecast PE underneath 2, c1/third of the market cap in money.

GKP with a c40% yield, PE underneath 2 and minimal extraction price – albeit with a extreme expropriation threat (for my part) – that I’ve managed to hedge.

My different oil and gasoline firms are in an identical vein. I’m not positive if it’s woke traders nonetheless not investing, or if they’re pricing in a extreme drop in oil costs. Most of those Co’s are very worthwhile at $70/oil and worthwhile all the way down to $50. With China re-opening and Biden refilling the strategic Petroleum reserve at $70 I can’t perceive why they’re buying and selling the place they’re. Others I maintain comparable to 883.hk, HBR, KIST, Romgaz usually are not as low-cost however I must diversify as these smaller oilers tend to undergo from mishaps, rusting tanks, manufacturing issues, rapacious governments and there aren’t sufficient of them round to allow them to make up the majority of the portfolio. At present I’m at 35% so a giant weight and which broadly hasn’t labored this yr over the time interval I’ve owned them. I received’t purchase extra and plan to restrict my measurement to c5% per firm.

We’ll see if these rerate in 2022. There’s a lot to dislike about them. Firstly, that they proceed to take a position regardless of being so lowly rated. Why make investments progress capex if you’re valued at a PE of two/3 and a considerable proportion of your market cap is money? Much better to only distribute / preserve manufacturing for my part. I discover it attention-grabbing that Warren Buffett insists on sustaining management of his firms surplus money circulate and exerts tight management on their funding choices while far too many worth traders are ready to present administration far an excessive amount of credit score and management.

The draw back to those firms investing to develop is they’re *typically* rolling the cube with exploration and its an unwise sport to play, as there may be a lot of scope for them to not discover oil/gasoline. Even when they purchase there are many dangerous offers on the market and scope for corruption at worst, or very dangerous resolution making at greatest. I dont belief or price any of the managements however the shares are so low-cost I’ll tolerate them for now / till I discover higher options. I additionally imagine corruption could also be why so many of those kind of shares are eager on capex initiatives – because it’s simpler to steal from a giant mission than ongoing ops. I’ve no proof/indication of any specifics for any particular firm and its very a lot supposition on my half…

It’s just a little irritating, after I look again to my begin 2022 portfolio I had loads of oil and gasoline – although far an excessive amount of was in IOG which I had a fortunate escape from. I seemed for extra in early 2022 however was searching for the highest quality oil and gasoline cos, which on the metrics I take a look at all occurred to be in Russia. Irritating to get the sector proper however not think about that every one my oil and gasoline publicity was in Russia so, in the end didn’t work out.

I’m not positive how a lot of this lowly valuation is all the way down to ESG / environmental considerations. I think this impacts it drastically. On the uncommon events I meet individuals new to investing, ESG is the very first thing they ask about and it’s actually necessary to many corporates – because it’s the favour du jour. I imagine it to be completely delusional – all the system is damaged and irredeemably corrupt and I’m ready to embrace this reality, somewhat than deny it. We’ll see if this works over the following few years, I think exhausting occasions will treatment individuals of the ESG delusion however we will see… The counter argument is that non-ESG firms can’t increase capital so usually are not as low-cost as they seem. I don’t imagine that is the case in the long term – the cynical will as soon as once more inherit the earth.

I’ve tended to get into the behavior of shopping for these shares on excellent news, anticipating this to set off rerating, then promoting on dangerous information, which comes together with stunning regularity. Aim for 2023 is to purchase as low-cost as potential then simply maintain. Promoting the tops seems interesting however as soon as it turns into clear that oil will not be going to $50 / ESG doesn’t matter then the rerating might be formidable, even a 5x money adjusted PE will give JSE / PTAL 100%+ when it comes to share value.

When it comes to my different useful resource co’s Tharissa remains to be very low-cost. I’ve traded just a little out and in with a minimal stage of success, although just like the oil firms they’re a inventory buying and selling sub-NAV on a tiny a number of and, after all, the conclusion they arrive to is it’s time to spend money on Zimbabwe, somewhat than a purchase again or return money by way of dividends. Sensible guys, good…

Kenmare can also be low-cost on a ahead PE of underneath 3, one of many world’s largest producers, on the lowest price and a ten% yield. The difficulty is that if we’re heading to a serious recession this may increasingly hit demand and pricing. However it could possibly simply be argued that that is within the value.

Uranium remains to be an affordable weight however its very a lot a gradual burner for me – I’m positive it will likely be very important for technology sooner or later however when the value will transfer to incentivise new manufacturing stays unknown. I nonetheless assume KAP is undervalued, although it hasn’t executed effectively during the last yr. In breach of my no sector ETFS rule I nonetheless personal URNM, very unstable however I’ve minimize the burden all the way down to a stage I can tolerate. The true cash in uranium might be probably made within the know-how / constructing the crops however nothing on the market I should buy – Rolls Royce simply seems too costly and there may be an excessive amount of of a historical past of huge losses occurring in the course of the growth of recent nuclear know-how.

One in every of my higher performers over the yr has been DNA2. This consists of Airbus A380s which had been buying and selling at a major low cost to NAV, after I purchased they had been buying and selling at a reduction to anticipated dividend funds. In an identical vein I’ve purchased some AA4 (Amedeo AirFour Plus). If dividends are paid as anticipated I hope to get about 20-30p a share over the following 5 years, then the query is what are / will the property be price? Emirates are refurbishing among the A380s so I believe there’s a respectable prospect they are going to be purchased / re-leased on the finish of their contract or not less than have some worth. We’re in a rising rate of interest atmosphere now and the price of airframes is a serious a part of an airline’s price. In the event that they purchase new at a c0-x% financing price then, maybe gas / effectivity financial savings make new planes worthwhile. This calculation modifications if they’re having to purchase new, with a better capital worth at a better rate of interest – making the used plane comparatively extra enticing and economical. There are additionally supply points throughout Boeing and Airbus, once more serving to the used market. Offsetting this, air journey will not be but again to 2019 ranges and a extreme recession / excessive gas costs could kill demand additional. Nonetheless my guess is on the A380s being price one thing and the A350s additionally having a little bit of worth, with a c16% yield in the event that they hit their goal, I receives a commission to attend, although a few of that is capital being returned, although its exhausting to say how a lot as we don’t actually understand how a lot the property are price.

Begbies Traynor is one other large weight however has not executed a lot, given it’s now elevated weight with the possibly everlasting demise of my Russian holdings. I believe it’s a helpful hedge to the remainder of the portfolio. It’s one I would like to chop on account of extreme weight.

I’m broadly amazed how robust every part is. UK vitality payments have risen to a typical c£4279 in January 2023. UK GDP per capita is roughly c£32’000 -post tax that is 25k so vitality is now 17% of internet pay. It is a large rise from c £1100 or 4% pre-war. The typical particular person/ family doesn’t pay this immediately – as its capped by the federal government at c£2500, that is, after all, not completely correct – the subsidy might be paid by taxpayers ultimately. I’m conscious I’m mixing family and particular person figures – however the precept applies a lot of cash is successfully gone. Varied windfall taxes can shift burden round a bit. Don’t neglect the median particular person earns underneath £32k – because of skew from excessive earners. If you happen to couple this with rising meals costs / mortgage charges and no certainty on how lengthy it will final and I’m amazed shares are as resilient as they’ve been. I think that is pushed by the hope that that is short-term. I’ve my doubts as to this.

I’ve tried a couple of shorts as hedges – broadly they haven’t labored. My principal guess has been to imagine the patron – squeezed by insanely excessive home costs / rents and mortgage charges, excessive vitality prices and rising tax would reduce. I’ve shorted SMWH (WH Smiths) and CPG (Compass Group). Sadly we’re nonetheless seeing restoration from COVID in yr on yr comparisons and there seems to be little fall off in client demand. It might be I’m within the mistaken sectors. SMWH do *largely* comfort retail at journey areas, CPG outsourced meals providers. I assumed these could be very simple for individuals to chop again on. For instance, bringing a chocolate bar purchased at a grocery store for 25-35p somewhat then shopping for one at SMWH for £1. This hasnt labored as but. Its potential individuals are chopping again on issues like garments somewhat than comfort gadgets / lunch on the workplace and so forth. This really makes plenty of sense because the saving from not shopping for that additional jacket equals many chocolate bars… I discover it very tough to anticipate what the common particular person spends on / will reduce on. I’m sticking with the shorts for now – these firms are valued at PE’s of 19 and 23, in a rising price atmosphere, I simply can’t see them persevering with to develop. However I’m approaching the purpose at which I might be stopped out. A extra optimistic quick is my quick on TMO – Time Out – very small, closely indebted, each a web based listings journal and native delicacies market enterprise, it was not creating wealth even earlier than inflation induced belt tightening. I may do with a couple of extra like this, however many appear to be on PE’s of 10, so while I believe they solely look low-cost because of peak earnings it’s not a guess I’m keen to make. I haven’t been in a position to become profitable shorting the Gamestop’s / AMC’s. I’m not wired to tolerate massive drawdown’s on a inventory that’s going up that I already assume it overvalued. Tempted to maintain going with small makes an attempt at this to attempt to study to be extra in a position to put my finger on the heartbeat of the gang and get it close to the highest. I’m much better at selecting the underside on a inventory.

I additionally shorted NASDAQ (Dec sixteenth 9900) by way of places – didnt work – although was in revenue a lot of the time… As well as, I switched a few of my money from GBP to CHF – just about on the low, at the moment down 5.7%. I’m not tempted to change again – I’ve no religion within the UK economic system – present account deficit of 5% – earlier than imported vitality price hikes actually kick in, coupled with a funds deficit of seven.2% of GDP. The remainder of the West isnt significantly better. This additionally explains my fairly wholesome weight in gold steel, I cant make sure the place the underside is and wish to maintain ‘money’, solely I don’t wish to maintain precise money as I’ve no religion my money wont be devalued so gold or a ‘exhausting’ forex comparable to CHF might be subsequent neatest thing.

When it comes to life this yr’s loss has been a serious blow. I used to be planning to give up the world of employment in early 2022, however the state of affairs is such that I’ve postponed it. If we assume my direct Russian holdings are a 0, I’ve gone from having c45 yr’s spending lined final yr to solely round 25 years, it doesnt assist that I used to be badly hit by the inflation – my consumption is closely meals / vitality based mostly. Undecided what the following steps are – I nonetheless work half time, in a reasonably straight-forward distant job however am more and more fed up of the world of employment. I do wonder if if I weren’t splitting my time I might have made the Russian error / put fairly as a lot as I did in. I used to be searching for a considerable fast win. For lots of years I’ve thought of transferring someplace cheaper than the UK, most likely Japanese Europe. The issue in the intervening time is this could contain pulling more cash from my considerably diminished portfolio in addition to a giant change in way of life. I’m ready for both the job to complete or my vitality co’s to considerably rerate – so I’m not leaving a lot on the desk after I pull out the funds to maneuver nation.

Detailed holdings are under:

There’s a little leverage right here, however loads of money / gold to offset this – so in impact it is a small guess towards fiat. I view it as really being c14.9% money.

I bought some BXP this yr as I used to be compelled to by my dealer dropping it from my ISA, I nonetheless prefer it.

I bought DCI, Dolphin Capital – after a few years of holding, I believe price rises have modified the relative image, with this buying and selling at a c 67% low cost to a probably unreliable NAV, while I should buy one thing like BBOX for a 42% low cost to NAV nevertheless it’s much more professional, and has strong cashflow. I don’t personal BBOX but – I’ll when/if I can decide it up for a a lot decrease money circulate a number of. After price rises I don’t completely belief the NAV’s of those co’s / realizability at this NAV. It’s a really completely different world at larger charges, significantly as charges proceed to rise. There’s a counter argument as inflation can increase the worth of some property / price rises could also be short-term nevertheless it’s not a guess I’m keen to make in the intervening time. I’m going to be searching for low-cost / bought off property however will worth it based totally on FCF / dividend yield.

When it comes to sector the break up is as follows:

I’m closely weighted in direction of pure sources / vitality, really it’s worse that as my Russian shares and my Romanian fund Fondul Proprietea are each closely pure useful resource / vitality value linked. There’s a highly effective counter argument – in that price rises kill demand and with it the marginal purchaser inflicting excessive useful resource costs – so a small lower in financial exercise may trigger a big fall in useful resource co costs. It’s a reputable argument and a part of why I pulled out from silver/copper miners (largely) in the summertime. My reply is that there’s nonetheless a scarcity of funding, lots of the shares I personal have massive money piles and excessive cashflow per share – they largely pay for themselves in two/ three years. In even an extended dip they need to do OK and provide shortages could imply they’ll rise out any recession – in 2008/9 vitality and sources carried out surprisingly strongly.

I’m going to restrict any additional weight to pure sources – although I’d change between shares, tempted to chop the extra mainstream oil and gasoline co’s in favour of extra unique holdings if I can discover shares of enough high quality.

Not in a rush to purchase something – except it’s actually low-cost or low-cost and low threat / fast return. Little or no on the market actually appeals, although I’m frequently drawn to Royal Mail as an honest enterprise, going by means of a tough patch that may probably rerate. I’d like to change money / gold into undervalued funding trusts / very low-cost companies with excessive margin’s and huge money piles, however, as ever, these appear to be exhausting to seek out.

As ever, feedback appreciated. All the very best for 2023!

[ad_2]