[ad_1]

The top of the federal pupil mortgage reimbursement grace interval has been a monetary impolite awakening for tens of millions of debtors. After the pandemic-related pause on funds since March 2020, the Division of Schooling’s 12-month “on-ramp” program, which quickly suspended penalties for missed funds, concluded on September 30, 2024.

As federal pupil mortgage funds resumed, many debtors couldn’t make their funds, indicating {that a} rise in delinquency and a return of defaults are anticipated in 2025. We’re now studying which sorts of debtors are have the toughest time making funds.

Survey: Many Scholar Mortgage Debtors Unprepared for the Finish of the Grace Interval

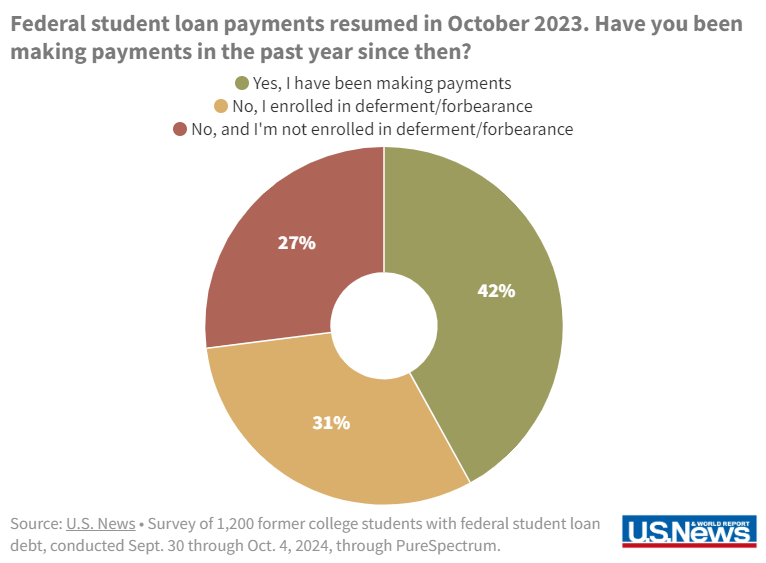

A latest survey revealed that solely 42% of pupil mortgage debtors are making common on-time funds. This places many susceptible to delinquency and default, significantly those that haven’t made funds or enrolled in deferment or forbearance.

The return of pupil mortgage reimbursement has triggered appreciable stress amongst debtors, with 86% experiencing some stress associated to their debt. Practically 1 / 4 of respondents described their stress ranges as “excessive.” Many debtors proceed to advocate for pupil mortgage forgiveness, with 77% supporting one other try and cancel pupil mortgage debt.

- 63% reported monetary hardship, with many struggling to handle different bills. Generally impacted areas embrace bank card payments (31%), housing prices (21%), and auto loans (17%).

- Over half (57%) have lowered financial savings, together with emergency funds and retirement contributions, to maintain up with funds.

- Alarmingly, 62% wouldn’t be capable of cowl a $1,000 emergency expense utilizing money or financial savings alone.

- 65% of debtors have adjusted their bank card spending habits, with some turning into extra reliant on credit score to fulfill every day bills.

Debtors with out Levels Struggling the Most

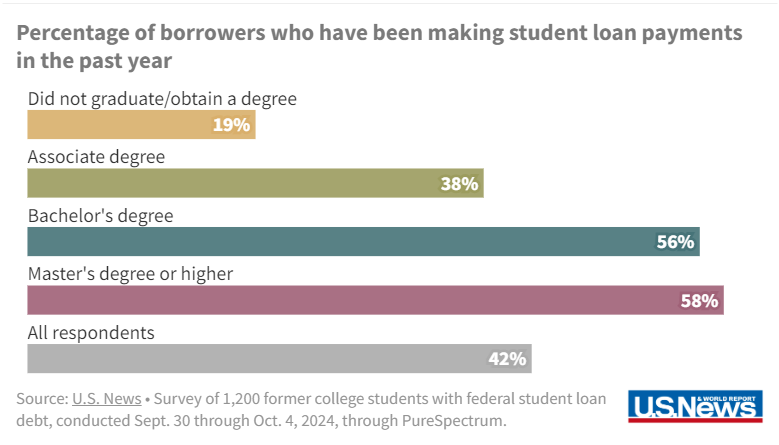

- Debtors with out levels are at a better threat of delinquency, with solely 19% having made any funds previously 12 months, in comparison with 50% of diploma holders. Moreover, solely 31% of non-degree holders had been conscious of the expiration of the “on-ramp” program.

Reaching out to non-completers is a chance for faculties to maintain these debtors from defaulting by re-enrolling them to finish their levels. A robust incentive to re-enroll is the in-school deferment, no pupil mortgage funds are required whereas they’re engaged on their diploma. After which, after commencement, they’ll be capable of earn more cash and afford their funds.

File-Excessive Defaults Anticipated

Now that the grace interval has ended, debtors face extra than simply credit score rating injury in the event that they miss funds. Loans can ultimately enter default, resulting in wage garnishment, tax refund offsets, and potential authorized penalties.

Faculties will even be held accountable via their Cohort Default Charges. Faculties that exceed the brink for defaulted debtors might threat dropping their Title IV lending standing.

Consequently, faculties want a robust Default Aversion program to assist educate debtors about their fee choices and information them into sustainable reimbursement plans together with income-driven reimbursement (IDR) plans.

Debtors must be notified when modifications in pupil mortgage insurance policies happen, particularly when it impacts their plans. Many debtors count on their loans to be forgiven and keep away from funds. They should be advised that they will make minimal funds via an IDR plan and nonetheless qualify for forgiveness with out risking delinquency. The SAVE plan remains to be below a court docket injunction, however different IDR paths have opened up.

Staying knowledgeable and taking proactive steps might help debtors handle their pupil loans extra successfully.

[ad_2]